America’s retirement landscape is undergoing a profound generational transformation. Baby boomers—once the largest and wealthiest generation in U.S. history—are increasingly finding themselves unable to retire on schedule due to soaring living costs, insufficient savings, and the erosion of traditional pensions. Meanwhile, a striking shift is emerging among the youngest adults: Gen Z is opening retirement accounts earlier than any generation before them, with some starting as young as 19, according to Robinhood CEO Vlad Tenev.

This widening generational contrast exposes both a deep structural divide and a powerful behavioral shift that could reshape the financial future of the United States.

1. Why Boomers Are Being Forced Back Into the Workforce

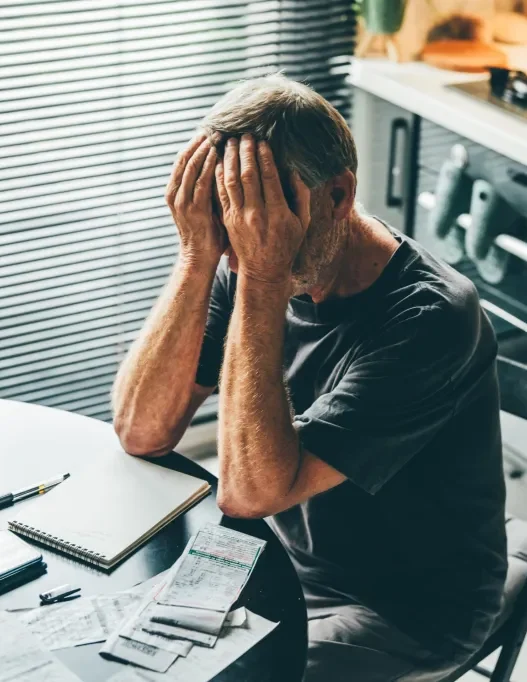

Despite decades of work, many boomers are reaching their mid-60s and early 70s without the financial cushion they expected. Several economic forces have combined to push them back into the labor market.

A. The Cost of Retirement Has Exploded

Over the past two decades, the cost of healthcare, housing, and consumer essentials has far outpaced wage growth. Retirees today face:

- higher Medicare premiums,

- rising rent or property taxes,

- expensive out-of-pocket medical bills,

- and a cost-of-living crisis accelerated by post-pandemic inflation.

The result: the classic retirement model—pensions, modest savings, and Social Security—no longer stretches far enough.

B. The Decline of Employer Pensions

In the 1980s, nearly 60% of private-sector workers had access to defined-benefit pensions. Today, that number is below 15%.

Boomers are the first generation to fully experience the transition from guaranteed pensions to 401(k)-style plans, where individuals shoulder all the risk. Many simply did not save enough or invested too conservatively for decades.

C. Market Volatility Eroded Savings

The dot-com bust, the 2008 financial crisis, and the 2020 market turbulence created repeated shocks to retirement portfolios. For boomers who withdrew funds or paused contributions during downturns, compounding suffered significantly.

D. Social Security Isn’t Enough

Social Security provides an average of around $1,900 per month—barely enough to cover housing in many U.S. cities, let alone medical care, food, or transportation.

For millions of boomers, retiring solely on Social Security is not feasible.

E. Rising Debt Among Older Americans

Boomers now carry record levels of:

- mortgage debt,

- credit card balances,

- medical debt,

- and even student loans from co-signing children’s education.

This debt burden forces many to extend their working years indefinitely.

The Outcome: Older Americans Are Working Longer Than Ever

The share of Americans aged 65 to 74 who are still working has doubled since the 1980s and is projected to rise further. Many are returning to work not out of passion—but necessity.

2. Gen Z: The First Early Retirement Generation

In stark contrast, Gen Z appears to be rewriting the playbook. Robinhood CEO Vlad Tenev recently revealed a surprising trend: Gen Z users are opening retirement accounts as early as 19 years old.

This is revolutionary within the American financial system.

A. The FIRE Influence (Financial Independence, Retire Early)

The FIRE movement, popularized on social media and among young digital-first communities, has inspired Gen Z to:

- pursue early savings,

- invest aggressively,

- minimize debt,

- and build long-term wealth.

Unlike boomers—who often learned investing later—Gen Z is absorbing financial literacy through TikTok, YouTube, and online forums.

B. Automated Investing Makes Early Retirement Planning Easy

Apps like Robinhood, Fidelity, and Betterment allow young adults to:

- open Roth IRAs in minutes,

- invest as little as $10 at a time,

- and automate monthly contributions.

The barrier to entry has collapsed, enabling teenagers and young adults to invest years earlier than previous generations.

C. The Power of Starting at 19

A 19-year-old investing just $150 a month at an 8% annual return could accumulate over $750,000 by age 65—even without ever increasing contributions.

Starting this early gives Gen Z an extraordinary compounding advantage over boomers, who often began saving in their 40s or 50s.

D. A Distrust of Job Security Drives Early Planning

Gen Z watched:

- their parents lose jobs in the 2008 crisis,

- students graduate into the 2020 pandemic recession,

- inflation erode wages,

- and automation threaten future employment.

This has produced the most financially cautious youth generation in modern history.

3. Two Financial Realities: One Country, Two Futures

The contrast between boomers and Gen Z reveals a growing generational divide in financial experiences.

Boomers:

- Dependent on pensions and Social Security

- Hit by multiple recessions in late career

- Burdened by rising healthcare costs

- Started saving later due to different economic norms

- Often financially unprepared for long retirements

Gen Z:

- Starting retirement accounts in their teens

- Using technology to automate investments

- Learning personal finance through social media

- Avoiding debt when possible

- More skeptical of long-term job stability

- Intent on achieving early financial independence

4. The Broader Economic Impact

This shift has profound implications for the U.S. economy.

A. Labor Market Dynamics Will Change

As boomers remain in the workforce longer, competition for jobs rises. Yet at the same time, their continued participation helps stabilize industries facing worker shortages.

B. Wealth Distribution Will Evolve

If Gen Z continues to save aggressively, they may accumulate wealth earlier than millennials or Gen X—potentially reshaping long-term economic power dynamics.

C. Retirement Systems Must Adapt

The U.S. will need to confront:

- Social Security solvency issues,

- the inadequacy of current retirement tax incentives,

- healthcare inflation,

- and rising longevity mismatched with financial preparedness.

5. A New American Retirement Reality Is Emerging

The traditional notion of retirement—working until 65 and living comfortably for two decades—is collapsing for millions of older Americans. At the same time, an entirely new model led by Gen Z is taking shape: retire earlier, invest sooner, and leverage technology to build long-term wealth.

The clash between these two trends encapsulates the broader generational transformations defining America’s economic future.

- Boomers are fighting for financial survival.

- Gen Z is preparing for financial independence before age 20.

- The retirement system is being reinvented in real time.

The divide is stark, but the lesson is universal:

The earlier Americans invest, the more control they gain over their future—and the more insulated they become from the economic shocks that now define modern life.